For most of M&A history, the pace of a deal process was constrained by a simple bottleneck: how fast a team could build conviction.

Conviction requires research. Research requires time. And time, in a competitive deal process, is rarely neutral.

What AI is changing is not the nature of that work. A rigorous investment thesis still demands the same intellectual inputs it always has: sector context, competitive positioning, management quality, financial architecture, risk factors. What is changing is how long it takes to assemble those inputs to a standard that supports a decision. And as that window compresses, the competitive dynamics of deal-making are shifting in ways that most teams have not fully reckoned with.

The old pace had a hidden cost

When a research sprint takes three weeks, teams adapt. They narrow scope. They prioritise the targets most likely to close rather than the targets most worth evaluating. They make early judgements about sector fit that become difficult to revisit. They miss opportunities through no lack of access, but because the cost of thorough evaluation was too high to apply universally.

This is a rational response to a resource constraint. But it means that many of the deals that never happened did not fail on their merits. They were never seriously evaluated. The true cost of slow research runs deeper than the hours. It is the decisions that were quietly narrowed before they were ever made.

Speed to conviction controls the process

In a competitive deal process, the team that arrives at conviction first has a structural advantage. They enter exclusivity discussions with a sharper view of value. They frame the terms. They define what due diligence confirms rather than discovers. The later team is reacting; the earlier team is setting the agenda.

This dynamic is not new. What is new is that the gap between the fastest teams and the slowest is widening, and it is widening faster than most organisations have noticed.

A corporate development team that can move from initial target identification to a board-ready investment thesis in days rather than weeks does not just save time. It reshapes its position in the process. It can engage earlier, with more credibility, and with a view of value that has been tested against more angles than a compressed timeline would previously have allowed.

The same is true in private equity. The funds building research capacity that allows them to evaluate more opportunities in parallel, at higher quality, are doing something beyond efficiency. They are changing what they see. They are finding conviction on targets that other funds have not yet evaluated seriously. That is a sourcing advantage, not just an operational one.

What this looks like in practice

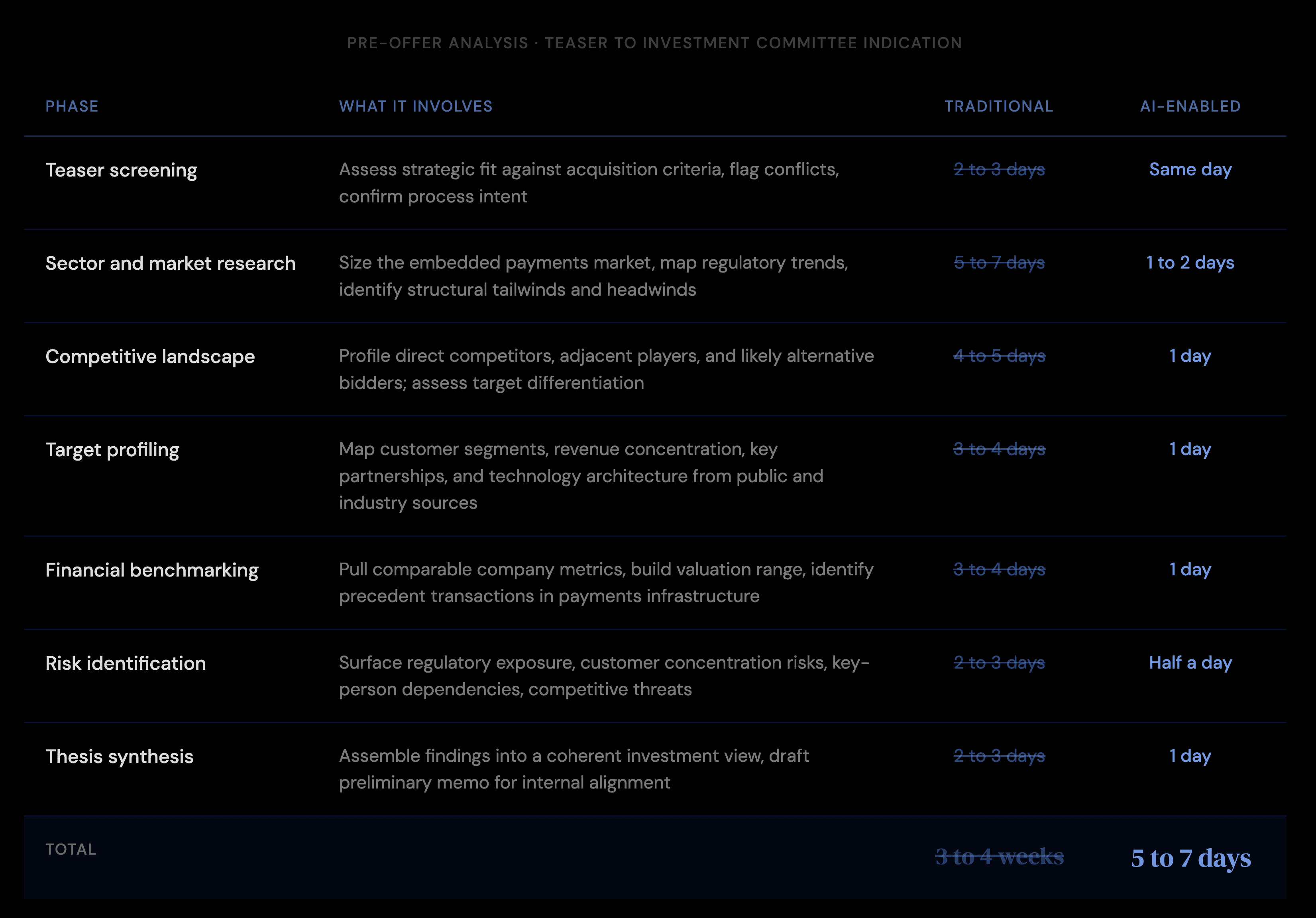

Consider a corporate development team at a diversified financial services group. They receive a teaser from an investment bank for a payments infrastructure business: a B2B platform processing embedded payment flows for mid-market lenders, around 180 employees, recurring revenue model, growing at roughly 30 percent year on year. The bank has set a process. First-round indications are due in 12 days.

The target may well be interesting. The question is whether the team can form a serious view in the time available. Both teams face the same analytical task. What differs is how long each phase takes.

In the traditional model, a 12-day process window is tight. The team can complete the work, but only by running phases in sequence, narrowing scope under time pressure, and presenting a view to leadership that has been insufficiently stress-tested. The indication submitted at day 12 reflects what the timeline permitted, rather than what conviction required.

In the compressed model, the same 12-day window is comfortable. The team completes its analysis by day seven and spends the remaining five days stress-testing the thesis, pressure-checking assumptions, and preparing leadership for questions the bank or sellers are likely to raise. The indication submitted at day 12 reflects a view that has been built, reviewed, and interrogated.

These two teams are submitting bids on the same target, at the same deadline, with the same publicly available information. The difference is what each team was able to do with the time they had. In a process where the sellers' advisers are reading every indication for the quality of thinking behind the number, that difference is not abstract.

Parallel capacity changes what is possible

The compression of individual deal timelines matters. But the deeper shift is in how many processes a team can run concurrently.

When thorough sector research takes weeks, the number of targets a team can seriously evaluate at any given moment is constrained. When it takes days, that constraint loosens significantly. The practical result is that AI-enabled teams are covering more ground, building richer sector maps, and returning to targets they would previously have set aside as too resource-intensive to evaluate rigorously.

This changes the quality of sourcing. A team that can run ten serious evaluations in the time it previously took to run three is developing a different and more complete view of its opportunity set. Over time, that view compounds. The sector knowledge built from evaluating more targets, across more market conditions, produces a research asset that becomes increasingly difficult for slower-moving teams to replicate.

That compounding knowledge is a sourcing advantage. But it is only accessible to teams that had the bandwidth to build it in the first place.

The new baseline is forming now

To be clear: AI leaves the judgment required to do deals well entirely intact. Conviction still requires synthesis, interpretation, and the willingness to reach a view that a data set alone cannot supply. Those remain human capabilities, and they remain the core of the work.

What is changing is the floor. The research standard that used to require three weeks to achieve can increasingly be reached in a fraction of that time. As more teams build or adopt the tools that enable this, that compressed timeline ceases to be an advantage and becomes the expected baseline. The teams that have adapted will find themselves with a structural advantage. For those that have not, the disadvantage arrives not from any deterioration in judgment, but from the pace at which that judgment reaches the table.

The competitive edge in M&A has always been asymmetric. Access, relationships, and sector expertise have historically been the sources of that asymmetry. Time to conviction is now joining that list. The question for any deal team is a straightforward one: in two years, when the compression of research timelines has become standard rather than exceptional, which side of that asymmetry will you be on?

Sector research, competitive landscape, target profiling, benchmarking, thesis synthesis. In days, not weeks. Book a demo at semaverse.ai

Related blogs

Semaverse Launches AI Intelligence Platform for Mergers and Acquisitions

Support for various content types such as articles, blogs, videos, and more. Rich text editor with formatting options for enhanced.

3rd Nov, 2025

Semaverse and PitchBook Partner to Deliver Context-Aware M&A Intelligence

Support for various content types such as articles, blogs, videos, and more. Rich text editor with formatting options for enhanced.

18th Feb, 2026

Semaverse Named in Top 100 UK Startups: Why the UK is the New Epicenter for AI-Driven M&A

Support for various content types such as articles, blogs, videos, and more. Rich text editor with formatting options for enhanced.

3rd March, 2026